From Burning Energy To Harnessing It

One of the most important change in history was the transition from human, animal and wood energy to fossil fuels. It allowed for industrialization and an explosion in population, as well as society’s capabilities as a whole.

It also caused pollution and is unsustainable due the non renewable nature of fossil fuels. And they are getting increasingly harder to obtain, with fossil fuels now having to be extracted from shale deposits or ultra-deep underseas oil & gas wells.

This is why an equally important transition is happening into renewable energies, especially solar and wind, but also geothermal and hydro power.

Projections are for renewables to rise quickly until 2050, mostly replacing coal. If more aggressive goals regarding climate change were to be adopted, an even quicker adoption of renewables would be needed to also replace gas and oil.

Source: EIA

Behind the growth of renewables is a quickly declining cost, bringing them into being competitive with fossil fuels and nuclear. This decline in costs has affected most renewable power sources, but none as strongly as photovoltaics.

Source: Research Gate

Top 10 Renewable Energy Stocks

This list was made to reflect the diversity of the sector, and is organized by market capitalization at the time of writing of this article.

China Power Co., Ltd. (600900.SS)

China Yangtze Power fully owns 110 hydropower generation assets in China, including the Three Gorges dam and in total, 5 of the 12 largest hydropower dams in the world.

Source: China Yangtze Power

Hydropower is currently by far the largest source of green energy in the world. China Yangtze Power is the largest electric power company in China and the largest hydropower company in the world, with 71.7 GW of total capacity installed.

The company also has hydropower businesses in Brazil, Sudan, Pakistan, and Malaysia, and wind power generation in Germany.

Thanks to its reliance on hydropower, China Yangtze Power is able to produce green energy with a high level of reactivity to grid and market demand, with only seasonable fluctuation in rainfall able to limit its ability to generate power on demand. This makes it a highly reliable producer, and one unlikely to have to make massive investments in energy storage or electric transmission to deal with intermittent production like for solar and wind.

So investors looking for the highest level of safety and little growth might be the most interested in China Yangtze Power. They should nevertheless be aware that weather patterns can strongly affect the company’s production levels year-to-year.

The quality of the company’s assets is somewhat tempered by the geopolitical tensions between the West and China, which could affect the stock price without the business case having changed.

Iberdrola, S.A. (IBE.MC)

Iberdrola is one of the world leaders in green energy generation, with 40 GW of renewable capacity (out of 60.7 GW of total capacity), and aiming for 52GW of renewable capacity by 2025.

The 2025 Strategic plan includes €17B in renewable power production, as well as €27B in electric networks.

Iberdrola also plans €3.4B in green energy projects like hydrogen and green methanol production, industrial heat, micro-hydroelectric, electric vehicle charging stations, etc…

Iberdrola operates mostly in Spain, with operations in the rest of Europe, North America, and Brazil.

Source: Iberdrola

Iberdrola’s dividend policy states that “shareholder remuneration shall be between 65 % and 75 % of the net profit attributed to the Company”.

Between its planned growth and dividends above 4% yield, Iberdrola is a good utility stock for investors looking for exposure to green energy while also wanting some stability and safety from scale.

Ørsted A/S (DNNGY)

The Danish energy producer has gone through a massive transformation, from 2006 when it produced 83% of its power from fossil fuels to 2022 with only 8% left over, and on track to reach 99% renewable production by 2025.

Source: Orsted

It was the first company to create an offshore wind farm in 1991, and it is currently operating the world’s largest wind farm as well.

Orsted has an installed renewable capacity of 15.4 GW, with 4.9 GW more under construction and a grand total of 30.6 GW installed and in projects.

Half of this power generation is from offshore wind farms, with the rest roughly equally split between solar and onshore wind farms. Most of the planned growth is in offshore wind generation. Orsted has wind farms in Denmark, the UK, Germany, the US, Taiwan, and Vietnam.

Orsted is a pioneer in wind power generation and still leading the charge in growing this sector. So it can be an interesting stock for investors looking for utilities benefiting from declining costs of wind power.

Vestas Wind Systems A/S (VWDRY)

Vestas is a designer, manufacturer, and installer of wind turbines. With a cumulated total of 166 GW installed, it made and installed more wind turbines than any other company. It currently services 146 GW of wind generation capacity.

The company has a project pipeline of 32 GW. It controls 35% of the wind manufacturing market excluding China, up from only 20% in 2010.

It also has more revenues and order margins than any of its competitors. It is also the only one with a (strongly) positive EBIT (Earnings Before Interests and Taxes), thanks to its economies of scale.

Source: Vestas

This leadership also translates into unique innovations. Most importantly, Vestas has recently unveiled a new epoxy chemistry allowing for full recycling of wind turbine blades. This should allow for the wind industry to turn into a fully circular value chain.

Source: Vestas

Due to its scale, technological edge, and higher margin, Vestas is a relatively safe investment in the wind power supply chain, with its turbines the best-in-class in the industry.

First Solar, Inc. (FSLR)

First Solar is the largest solar panel manufacturer in the USA and in the whole Western hemisphere, with manufacturing sites in the US, Malaysia, and Vietnam.

The company is not using the classic crystalline silicon technology, and instead uses its proprietary thin-film photovoltaics. Based on cadmium-telluride, they are more efficient, are produced at a lower cost, and can be easily mass-manufactured. Thin-film solar panels are also more durable, retaining 89% of the original performance after 30 years.

Source: First Solar

Cadmium and telluride are byproducts of the mining for other metals, which means that First Solar products have a minimal environmental impact, using resources that were of little use before. Thin-film panels can also have high recycling rate.

First Solar’s technological edge, combined with its geographical location, makes it the likely beneficiary of the growing push for Western countries to source their panels from out of China. The company is ramping up its production capacity quickly, aiming to reach a capacity of 16 GW, from the current 8 GW.

This makes it a good stock for investors betting on continuous innovation in the solar sector, with thin-film the potential new generation of panels replacing silicon-based technology.

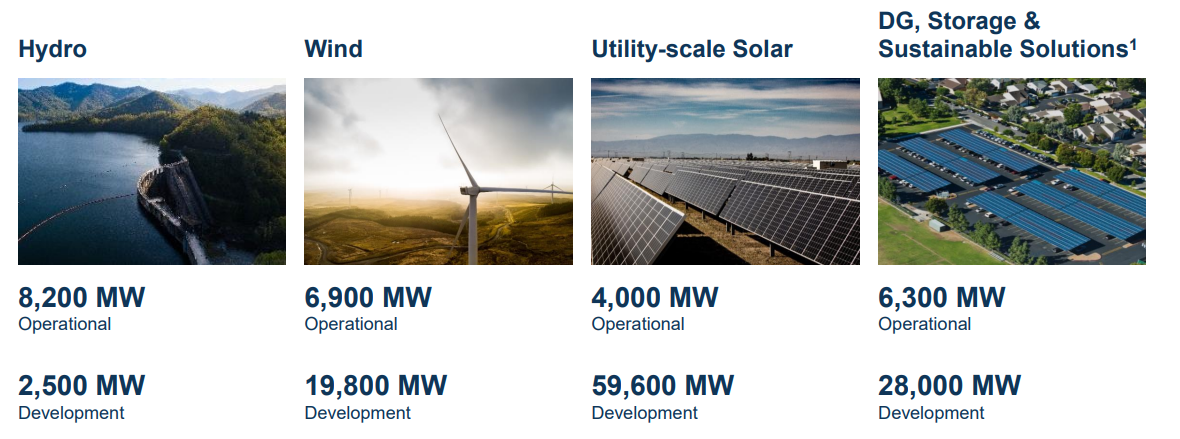

Brookfield Renewable Partners L.P. (BEP)

Brookfield Renewable Partners, or BEP, is part of the massive asset management firm Brookfield, handling $625B in assets, which owns 48% of BEP.

The company is managing 25 GW of power generation, and has a staggering 110 GW in its construction pipeline. Most of this growth will be in North America, with 71.2GW planned, mostly in the USA.

The current assets are a mix between hydropower, wind, and solar, with the bulk of the future production growth planned to be in solar, followed by energy storage and wind. Just for the next 5 years, BEP is planning to deploy $6-7B in new energy infrastructures.

Source: BEP

Another important development for BEP in 2023 is the closing of the acquisition of Westinghouse, the leading nuclear plant builder in North America. Westinghouse is an OEM (Original Equipment Manufacturer) for half of the world’s nuclear reactor fleet, and the immense majority of non-Russian /non-Chinese nuclear power plants.

Done together with the world’s second-largest uranium miner Cameco, this 7.9B acquisition will increase the role of nuclear in BEP’s revenues stream, even if more in the form of construction contracts than power plants and electricity sold.

While nuclear is not technically renewable, this shows the growing role of low-carbon nuclear in the energy transition and reflects positively on BEP’s management’s ability to follow business trends instead of a strict adherence to dogmas on energy policies.

BEP has grown its distribution to shareholders by 6% per year since 1999. Together with the rising stock price, BEP has generated annualized returns of 16% for its shareholders since 1999.

With its balance mix of hydropower, wind, solar, and now even nuclear, BEP is a solid stock to bet on the de-carbonization of the energy grid though various methods. It also has an excellent track record and distributes a rather generous dividend.

Ormat Technologies, Inc. (ORA)

Hydro is the legacy renewable energy, on which solar and wind are quickly catching up. But there is 4th way to generate green power, with is geothermal. It relies on the differential between the Earth’s surface and internal temperatures.

Progress in drilling technology, ironically partially linked to the oil & gas drilling technology, is now making geothermal an increasingly good source of economically viable energy.

Ormat is the 2nd largest geothermal owner and operator, and the largest publicly traded. The company has assets in the US, Kenya, Indonesia, and Central America+Caribean, with a capacity of 1.07 GW.

Source: Ormat

Ormat is also entering the energy storage market, with 104 MW to come online in 2023 and another 204 MW in construction. The company is aiming to reach a capacity of 1.8 GW by 2025 (including storage and solar).

Revenues grew by 10.7% in 2022, maintaining a strong growth trajectory since 2017.

Ormat’s aggressive growth targets are supported by the Inflation Reduction Act, which should provide up to $150M reduction to the company’s capital need for its geothermal and energy storage projects.

Sun and wind might at some point hit a threshold where their intermittency forces operators to add storage, potentially halting the cost reduction of these renewable energies. In comparison, geothermal is more able to provide stable baseload power and benefit from quickly improving technology, being just at the beginning of its development at the utility scale.

This makes Ormat a good pick for investors looking for low-carbon energy producers, but who might be wary of the long-term risks carried by wind and sun intermittency. With nuclear slow to develop and fossil fuel being phased out quickly, it is likely the stable and predictable production of geothermal plants will command a premium in the electricity markets.

Shoals Technologies Group, Inc. (SHLS)

Shoals is specialized in EBOS (Electrical Balance of System), or all the systems surrounding the solar panel themselves and which a required to make it work. This does not include inverters, but cables, switches, fuses, electric boxes, etc…

This segment benefits from the growth in solar installation, while not being under the same pressure for cost reduction as the panels themselves. This is because they represent less than 6% of the total system cost, with no component above 1% of the total cost. The sector also benefits from the retrofitting of older solar installations, as well as extra connection to new systems like batteries and EV chargers.

Source: Shaols

At the same time, suppliers are unwilling to take any chance with less reputable suppliers, as even very cheap components can cause catastrophic failures like fire, injury, or death. So this is a sector where established providers have a solid economic moat in the form of substitution costs.

Finally, Shaols’ unique offer is the pre-assembled “Plug’n’Play” system, allowing solar installations to be assembled without costly and hard-to-hire licensed electricians. This innovation is protected by 66 patents “limiting competitors’ ability to develop products that can replicate the benefits provided by Shoals”. The same concept is now being deployed for EV charging stations.

Between 2020 and 2022, Shaols has grown its revenues by 36% CAGR and its gross profit by 40% CAGR.

Source: Shaols

By focusing on a niche market with less innovation and competition than inverters or solar panels, Shaols has carved a profitable business line for itself that is now well established.

This might be appreciated by investors looking for a “pick and shovel” stock in the solar industry and unwilling to bet on a specific technology regarding the more contested battlefield for innovation on solar panels, inverters, or batteries

Daqo New Energy Corp. (DQ)

This Chinese company is one of the world’s leaders in polysilicon production, the central component for solar panel manufacturing. This also makes Daqo one of the founding pillars of China’s domination over solar panel manufacturing.

Daqo being at the center of the solar panel supply chain made it benefit greatly from the sector growth, with revenues growing from $0.68B in 2020 to $4.6B in 2022. After a surge in 2022, polysilicon prices have now cooled down.

The company’s communication and website are a little lackluster, but not out of character for an industrial B2B company, more focused on its image inside the industry than with the larger public or foreign investors.

In 2023, the stock is trading very cheaply compared to P/E or cash flow. This is partially due to controversies, with the company linked to the use of forced labor in Xinjiang, and talks in Washington DC of additional sanctions against companies operating in the region.

So investors should be aware that Daqo stock carries a very real geopolitical risk, as well as a large upside due to low valuation multiples.

JinkoSolar Holding Co., Ltd. (JKS)

Jinko is one of the largest solar panel manufacturers in the world, based mostly in China. The company is diversifying its manufacturing base, with silicon wafer manufacturing in Vietnam, and solar cell manufacturing in Malaysia and the US.

Jinko has delivered in the company’s whole history a total of 130 GW of solar cells, and aims for no less than 60-70 GW deliveries in 2023 alone. Module shipments to China have doubled year-to-year, and increased 50% for Europe.

Jinko’s most advanced solar cell, the N-type, achieves a remarkably high 25.8% energy efficiency. In 2023, the N-type is expected to take over most of Jinko’s sales, representing 60% of the whole.

The company has seen a decline in total shipments in Q1 2023, but with Q2 2023’s shipments are expected to climb back to the all-time highs of Q4 2022. Gross margins have stayed stable at around 14%-17%.

Source: Jinko

So this is stock mostly for investors looking to capitalize on the growing demand for solar, for China to stay at the center of this industry supply chain and for polysilicon panels to stay the main technology.

The post Top 10 Renewable Energy Stocks To Invest In appeared first on Securities.io.